Figure 1: General Overview of the Semiconductor Supply Chain

Being one of the most complex supply chains in the world, the semiconductor supply chain is worth around $0.5 trillion and is often very difficult to understand and manipulate. But before we dive deeper, we need to know what a supply chain is and how it impacts the world around us.

A generic supply chain is basically a system of organizations, corporations, people, activities, resources, and information, which is involved in offering a product or service to its’ customers. This means taking raw materials and processing them multiple times until they are in the right configuration and composition, making the final finished product that is delivered to the end customer. In the semiconductor supply chain, the output is a chip. This chip could be used in your mobile phone, car, or TV set.

Coming back to the semiconductor supply chain, it is extremely large and changes a lot over time as newer technologies are researched and older materials or techniques are exchanged for better ones. For context, the production of a single computer chip can require more than 1000 steps and close to 70 international border exchanges before it reaches the end customer.

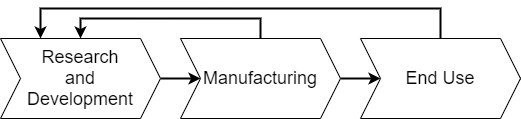

Figure 2 – Semiconductor Supply Chain

First of all, there are three main sectors to the semiconductor supply chain: research and development, manufacturing, and end use. There is a new sector coming more and more into the picture, recycling, which is expected and needs to become an integral part of future semiconductor production plants if we are to meet the global green future standards.

The first sector, research and development (R&D), is the powerhouse behind the entirety of the semiconductor supply chain, as new research ideas and technologies directly impact all the other involved sectors. R&D includes both pre-competitive, exploratory studies and research on the fundamental technologies, and competitive research, which is more aimed at advancing the leading edge that the company has in the semiconductor industry.

Secondly, production or manufacturing consists of five major steps: design, fabrication, assembly, testing and packaging, with the last three usually being coupled together under the acronym ATP and often done by an OSAT company.

Companies have two possible routes that they can take: do everything in-house, i.e. being vertically integrated, in which case they become IDMs (Integrated Device Manufacturers) and sell the chip themselves; or design a certain IC and then outsource the rest, fabrication to foundries and ATP to OSAT (Outsourced Semiconductor Assembly and Testing) vendors, making them a fabless firm. For example, Intel is an IDM and AMD (their direct competition) is a fabless company, as they design products, but do not have the capabilities or facilities to manufacture them.

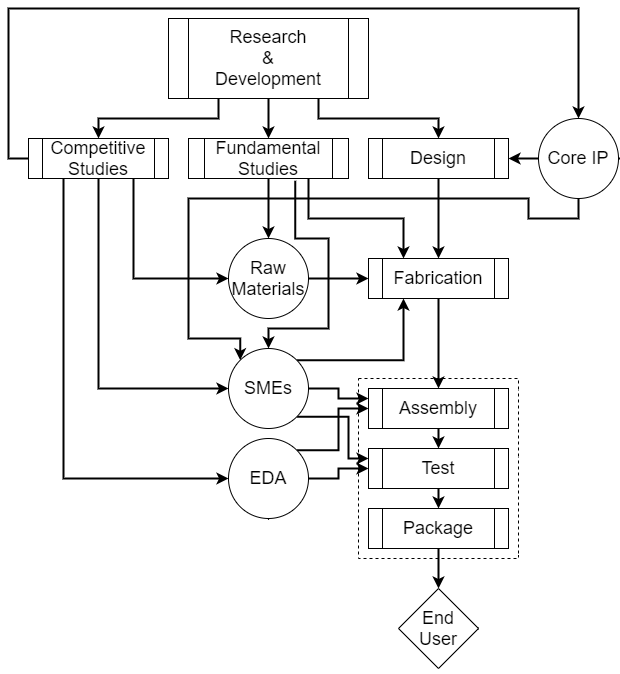

Regarding the inputs, the production of semiconductors has the raw materials, Semiconductor Manufacturing Equipment (SME for short), Electronic Design Automation (EDA) and the core Intellectual Property (IP).

Figure 3 – Detailed Semiconductor Supply Chain

As for end user, this involves distributing the ICs to other companies or retail customers for integration within a product (like smartphone, laptop, automobile, server, appliance etc.).

At the moment, the supply chain is spread between multiple companies on different continents, but is soon to change, as China enters heavily and fast on the semiconductor market in general, pushing to take over as much of the supply chain as possible.

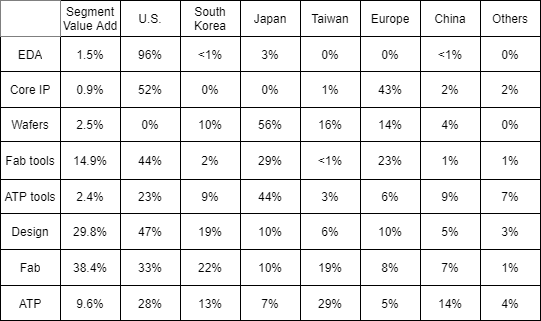

Figure 4: Semiconductor value add and market shares by segment and firm HQ

(source: CSET calculations, financial statements, WSTS, SIA, SEMI, IC Insights, Yole, and VLSI Research)

Currently, China lags behind overall, but is progressing in certain segments. It excels at ATP, with its excellent tools for assembly and packaging, and the production and refinement of raw materials. It has moderate, but growing, capabilities in design, fabrication, CMP (Chemical Mechanical Planarization, also known as polishing) tools, and some etch and cleaning tools. China faces challenges in other segments, though, like SME, with its greatest weaknesses being in EDA, core IP, fab materials, and bleeding-edge logic foundry capacity.

The other major player is the United States (taken with its allies), which is strong in most segments. Noteworthy exceptions include the production of some fab tools such as lithography equipment and materials including wafers. The United States also lacks leading-edge pure-play logic foundries. A semiconductor foundry is a fabrication plant that makes chips for third-party customers, unlike U.S.-based Intel, whose leading-edge logic fabs make chips based on Intel’s own chip designs. However, these capabilities are all dominated by U.S. allies. Taken together, the United States and its allies are internationally competitive in every segment in the supply Chain.

The United States decisively leads all other countries (including China) in the semiconductor research and development segment, which feeds into all other supply chain segments. The private sector performs most semiconductor R&D.

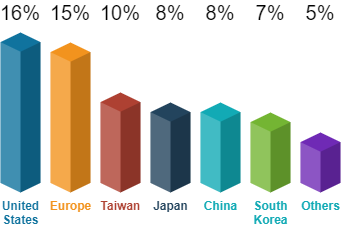

Figure 5: R&D as % of semiconductor devices sales

(source: CSET calculations, financial statements, WSTS, SIA, SEMI, IC Insights, Yole, and VLSI Research)

Over the next ten years, the industry will need to invest about $3 trillion just in R&D and capital expenditure globally across the value chain in order to meet the increasing demand for semiconductors.

While geographic specialization has served the industry well, it also creates vulnerabilities that each region needs to assess in a manner specific to its own economic and security considerations. There are more than 50 points across the supply chain where one region holds over 65% of the global market share, although the level of risk associated with each of these varies.

Manufacturing emerges as a major focal point when it comes to the resilience of the global semiconductor supply chain. About 75% of semiconductor manufacturing capacity, as well as many suppliers of key materials—such as silicon wafers, photoresist, and other specialty chemicals—are concentrated in China and East Asia, a region significantly exposed to high seismic activity and geopolitical tensions.

Furthermore, all of the world’s most advanced semiconductor manufacturing capacity—in nodes below 10 nanometers—is currently located in South Korea (8%) and Taiwan (92%). These are single points of failure that could be disrupted by natural disasters, infrastructure shutdowns, or international conflicts, and may cause severe interruptions in the supply of chips.

Industry participants and governments must collaborate to continue facilitating worldwide access to markets, technologies, capital, and talent, and make the supply chain more resilient.

The solution to all these challenges is not the pursuit of complete self-sufficiency through large-scale national industrial policies with a staggering cost and questionable execution feasibility. Instead, the semiconductor industry needs nuanced, targeted policies that strengthen supply chain resilience and expand open trade while keeping closely in view the needs of national security.

In addition, governments with significant national security concerns should establish a clear and stable framework for targeted controls on semiconductor trade that avoid broad unilateral restrictions on technologies and vendors.

In setting policies to promote supply chain resilience, governments must guarantee a level global playing field for domestic and foreign firms alike, as well as strong protection of IP rights. They must also take steps to further promote global trade and international collaboration on R&D and technology standards.

On the other hand, policymakers need to step up efforts to stimulate basic research and address the shortage of talent threatening to constrain the industry’s ability to maintain its innovation pace. To that end, further public investment in science and engineering education is needed, as well as immigration policies that enable leading global semiconductor clusters to attract world-class talent.

Such well-modulated policy interventions would preserve the benefits of scale and specialization in today’s global supply chain structure. This would ensure that the industry can extend its ability to deliver the continual improvements in semiconductor performance and cost that will make the promise of transformative technologies such as AI, 5G, IoT, and autonomous electric vehicles a reality in this decade.