The historic Apollo 11 spacecraft, which placed the first human on the moon, was powered by a computer that weighed 70 pounds, had 64 kilobytes of memory, and a few tens of thousands of transistors. Compared to this, an average smartphone with a couple of gigabytes of RAM and the equivalent of a few billion transistors squeezed into a device that weighs about five ounces would be millions of times more powerful. This story of the humble smartphone captures the beauty of developments within the semiconductor space.

While the progression of technology has been on a steep upward trajectory in recent years, the COVID-19 pandemic has accelerated the process further, and this will have distinct implications for the semiconductor industry. To help us identify some of the trends and factors that will shape the semiconductor landscape’s future, we invited Wally Rhines for a session on CXO Cyience with Suman Narayan, SVP of Cyient’s Semiconductor business. A leading voice on semiconductor and electronic design automation, Dr.Rhines is currently the CEO Emeritus of Mentor, a Siemens Business, and the CEO and President of Cornami, Inc. And these are some of the key insights and themes that emerged from our discussions.

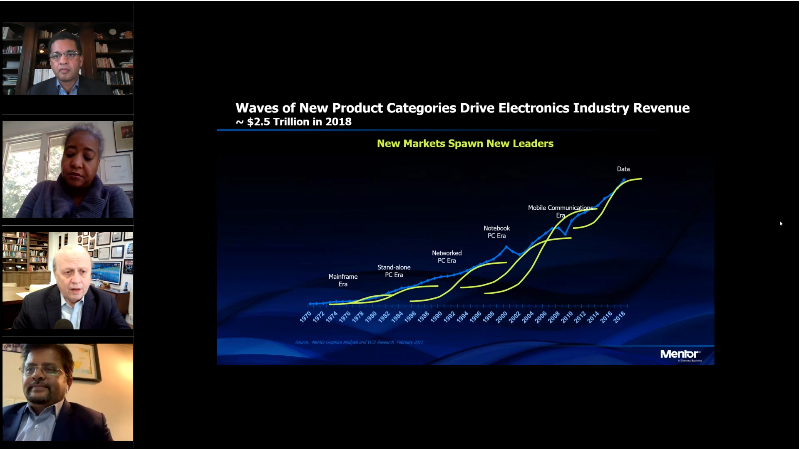

The data economy requires a new architecture

There is little doubt that we are increasingly moving toward a data economy where data is the new oil. Fueled by the growth of connected devices and social media, we are likely to generate more than 40 zettabytes of data by the end of this year and about 175 zettabytes by 2025. This, combined with the evolution of AI and 5G, will only increase the amount of data available. These unprecedented levels of data open a whole new world for businesses that are able to harvest this data effectively and in a secure manner to protect individual privacy. And as these applications grow, so will the demand for processing capacities.

For example, our ability to anonymize medical health records through Fully Homomorphic Encryption (FHE) will allow medical professionals and researchers to use the data more effectively without compromising individual privacy. As such applications become mainstream and we move to a new data and computing environment, we will require a new architecture that necessitates a huge computing capacity—a million times the performance of today’s best servers. And this is where a new generation of semiconductors will come to the fore.

Crises and the semiconductor industry share a unique relationship

Major economic and global crises share a straightforward correlation with the performance of most traditional business sectors. While most businesses register downward trends on key metrics during a crises, a look at the semiconductor industry’s history tells us a different story. For instance, while the global sales of semiconductors during the second quarter of 2020 decreased by 0.9% compared to the first quarter, it is a year-on-year increase of 5.1% from Q2 2019. In a pandemic year, when the worldwide economy is expected to contract, these are fairly robust numbers.

It is a similar story in terms of employment in the sector. Data from the US Department of Commerce indicates that unemployment among electronic and software engineers during Q1 2020 was well below the critical 4% threshold, which is used to define full employability. And counterintuitive as it may sound, it suggests a healthy demand for talent within the sector.

And finally, if we look at R&D spend in the semiconductor industry, data for the last 35 years reveals an average spend of 14%. And barring a single period from 2008-2009, the overall spending has grown every single year, irrespective of slow growth, flat revenues, and everything else that has happened during this period.

Democratization of technology and new applications are fueling growth

The latest numbers from the World Semiconductor Trade Statistics (WSTC) predict the worldwide semiconductor sales to be $426 billion by the end of this year. While this will be the second consecutive year of negative growth since 2018, it is critical to remember that it is still a year-on-year growth of 3.3% over 2019, a year during which the industry experienced a sharp fall in memory prices. More importantly, for us, the industry is expected to stage a comeback in 2021 with a projected growth of 6.2%. So, where is the growth coming from?

A significant area of growth (sales) for semiconductors in the last couple of quarters has been in the computing segment. Enabling work-from-home for tens of millions of people across sectors and countries has spurred the demand for servers, laptops, and the cloud. On the consumer and household side, besides becoming a requirement for remote education, PCs and laptops have become the primary means for entertainment, a big chunk of which includes e-gaming.

Going forward, the demand for servers is expected to remain very strong. The semiconductor revenue from the wireless segment is also expected to be relatively stable, primarily due to the 5G rollout, which will create a new market for smartphones that will have a significantly higher proportion of semiconductors.

We are entering a new age of specialization in semiconductors

The last few years have witnessed the emergence of non-traditional chipmakers who are creating a niche for themselves within the larger semiconductor ecosystem. On the one hand, the likes of Tesla, Apple, and Google are becoming vertically integrated to get better control over the product lifecycle and user experience. Today, these system companies account for nearly 20% of the wafer purchases from the foundries, and this is growing at 35% annually. On the other hand, companies in sunrise sectors like automotive and healthcare are developing new applications (electric cars) and creating products that never existed earlier (ingestible medical devices). In both cases, companies are developing these capabilities in-house and from the ground-up.

A case in point is the automotive sector, which has over 500 companies working on electric vehicles and over 275 on autonomous drive programs. As a result, the automotive sector consumes 9% of all ICs manufactured today, making it the fastest-growing application. Similarly, other emerging segments, such as healthcare, AI, and IoT, also require innovation in chip design and electronic components. This gives rise to ecosystems within the ecosystem that cater to application-specific needs and will result in the proliferation of players within the segment.

Here is the complete CXO Cyience session with Wally Rhines, where he also discusses the key themes from his recent book – ‘Predicting Semiconductor Business Trends – After Moore’s Law’.

About Suman Narayan

Suman Narayan heads the Semiconductor business unit at Cyient. In his current role, he is responsible for shaping and executing the business strategy for the unit, while growing key customer relationships.

Suman has over 20 years of experience in the high-tech electronics and semiconductor industry and has served in various leadership roles at ON (Fairchild) Semiconductor and Texas Instruments. In his last role he was the V.P at On semiconductors. Prior to that he lead Texas Instruments embedded processing group developing CPU’s for Automotive ADAS and Industrial applications for 19 years. He has several patents in signal processing and is an active member of the Semiconductor Industry Association.