“Automotive is the new El Dorado for microelectronics,” announces Emilie Jolivet, Director, Semiconductor & Software at Yole Développement (Yole). The market is showing significant market drivers that are daily supporting the growth: electrification, connectivity, autonomy and comfort are the key words of the today’s automotive industry.

Under this dynamic context, the market research and strategy consulting company releases a comprehensive technology & market report focused on advanced packaging solutions for automotive electronic components.

Titled, Trends in Automotive Packaging, this study identifies and analyzes the major platforms currently used in the automotive industry and points out technical trends related to LiDAR, CIS, radar, power and lighting devices, MEMS and sensors. Yole’s Semiconductor & Software team shares with you their advanced packaging knowledge applied to the automotive sector.

“For the first time, we clearly see packaging innovations for automotive components,” comments Emilie Jolivet from Yole. “Step by step, advanced packaging technologies initially developed for consumer purposes are implemented by Tiers 1 and 2. And the diversity of automotive components is a strong business opportunity for the advanced packaging companies.” Therefore, for the first time, the automotive industry is ready to accept consumer solutions, even for more dedicated applications like powertrain.

Based on the impressive growths of this industry (+7% for automotive sale – +15% for the electronics systems in automotive – And +20% for semiconductors in automotive…), Yole’s report highlights the attractiveness of this historic industry.

Automotive industry: where is advanced packaging implemented? What is the impact of regulations on these solutions? Who are the big advanced packaging big players? The Semiconductor & Software team from Yole invites you to discover the latest advanced packaging trends for the automotive industry.

Electronic devices are more and more common in cars and the number of electronic systems is also increasing. The quantity of electronics in a car has increased 2.5 times since the 90’s. In 2017, 26 cm² of semiconductor substrates was used in a car, while in 2023 Yole expects 35 cm². The four main trends empower the strong diversity of functions and so a large number of sensors, power supplies, communication chips, lighting components and processors that can either come from the consumer market or be especially developed for automotive.

“As an example, almost all OEMs have announced large investments or electrification plans of their fleet in the coming years,” comments Lauranne Chemisky, Technology & Market Analyst at Yole. “Impact of electrification should be first limited. Then, at long term, the story should be different. Automation and sensors guide innovation in the automotive industry, especially packaging solutions.”

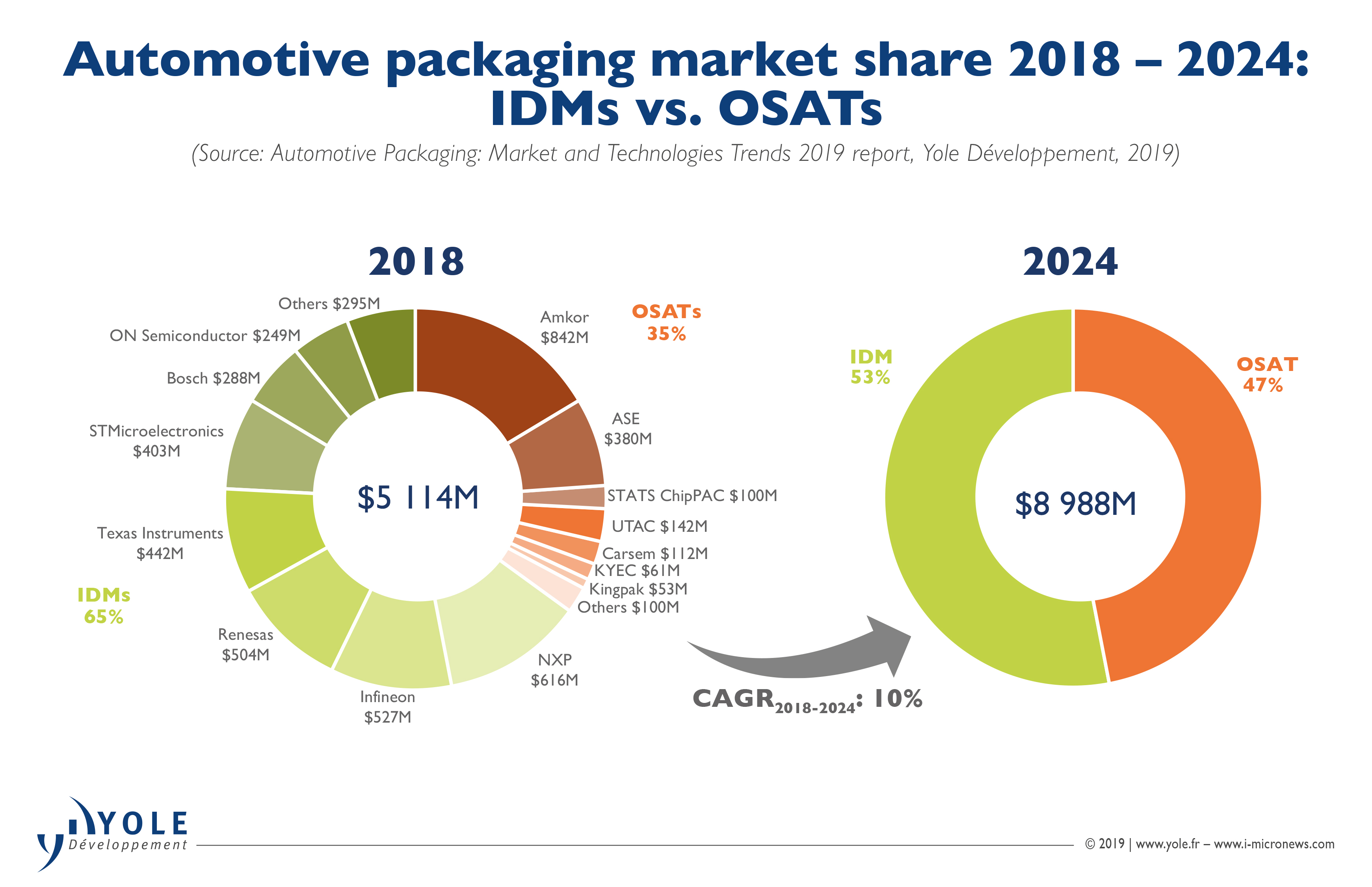

This impressive increase in electronic devices integrated in vehicles will directly drive the packaging market. In 2017, the packaging for automotive total revenue was quoted at about US$3.7 billion. According to Yole, it will reach roughly US$7 billion in 2023. The automotive packaging industry is involved in many device types and thus in many packaging platforms: the largest volume growth appears in power module, high power discrete and CIS markets. From a revenue point of view, LED is showing the highest figure and in parallel, LiDARs has the highest growth…

Yole’s team identified five main application groups with very different needs and operating conditions: infotainment & comfort, powertrain, safety, lighting and connectivity. Electronic devices can be either specific to one application group (Example: LEDs for automotive lighting applications) or be part of several groups, but with specific specifications. MCUs is a good example for the safety and infotainment applications.

Packaging affects how, where and how long the device can function… Yole’s analysts identified a new era for automotive development that may accelerate the adoption of innovative packaging technologies. “At Yole, there are today significant demands for power applications,” explains Emilie Jolivet from Yole. “A second wave could be led by new advanced packaging needs like embedded chips and more computing on the edge.”

In addition, for the first time in history, a big effort is made to adapt consumer technologies to the automotive sector. Although the main platform in term of units is the WBBGA package, which represents half of the market, advanced packaging platforms such as flip-chip and fan-out are finding their place.

The next packaging innovation expected is embedded die in substrate for converter dies. Packages like QFN package, iBGA Package and ceramic packaging are also growing for specific applications like CIS, MEMS and power devices.

These results will be presented by Santosh Kumar, Principal Analyst & Director Packaging, Assembly & Substrates, Yole Korea at the 20th Electronics Packaging Technology Conference (EPTC). This presentation will take place on December 5th at 4:00 PM during the Plenary Session 2, titled Packaging for next generation automobiles/autonomous vehicles. Make sure to attend this presentation and discuss with our expert. Feel free to visit also our team in the exhibition area (Booth #19).

A detailed description of the automotive packaging report from Yole is available today on i-micronews.com, advanced packaging reports section. All the types of packages used in the automotive industry, in addition to technology roadmaps are well detailed in this technology & market analysis.

Source: www.yole.fr