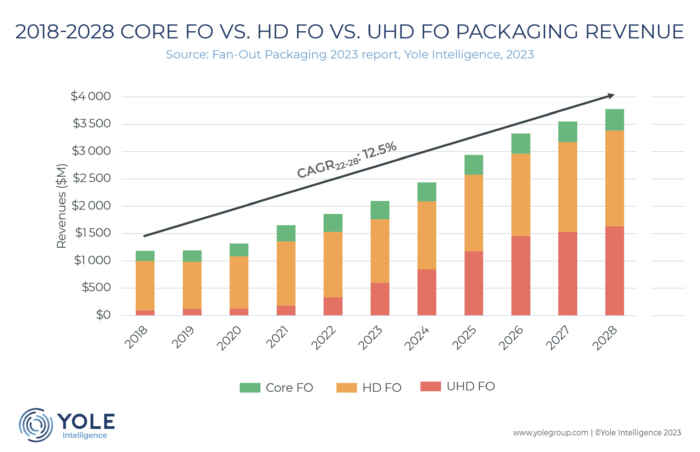

FO packaging revenue was US$1.86 billion in 2022. Yole Intelligence, part of Yole Group, expects it to have a CAGR of 12.5% through 2028, reaching US$3.8 billion. UHD FO will experience the fastest growth across all market classes, with a CAGR of 30%, growing from US$338 million in 2022 to US$1,630 million in 2028.

Gabriela Pereira, Technology and Market Analyst at Yole Intelligence, says: “HD FO is the dominating market class in 2022 with US$1,194 million in revenue, and it will have a 6.7% CAGR, reaching US$1,757 million in 2028. Core FO will have a 2.8% CAGR, increasing from US$329 million in 2022 to US$389 million in 2028. FO WLP volume will still dominate the market, with wafer production of 2,376K in 2028, versus 238K 300 mm wafer equivalent production for FO PLP . Total FO package volume will grow from 2,348 million units in 2022 to 2,960 in 2028. TSMC is the biggest FO packaging player, with 76.7% of the market”.

Indeed, as Yole Intelligence’s analysts affirm, the top three OSAT companies, ASE, Amkor, and JCET, together with TSMC, had more than 90% of the fan-out market in 2022.

In this context, Yole Intelligence releases its semiconductor packaging report, Fan-Out Packaging 2023. In this report, the company – part of Yole Group – identifies and describes which technologies can be classified as FO packaging and defines market classes. It also analyzes key market drivers, benefits, and challenges of FO packages for the different applications, the different existing technologies, their trends, and roadmaps and analyzes the supply chain and fan-out packaging market landscape. In addition, this report provides a market forecast for the coming years and estimates future trends.

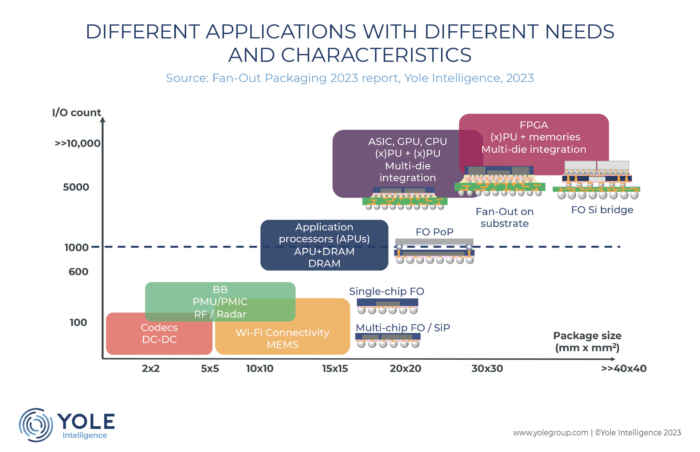

FO packaging has evolved from a low-end packaging technology into a high-performance integration platform, with growing adoption in the HPC , networking, automotive, and high-end mobile markets. One of the major market trends driving fan-out packaging technology is large die partitioning into chiplets and heterogeneous integration. Fan-out is a cost-effective platform that enables high-bandwidth and high-density die-to-die interconnections through RDL -based processes. UHD FO will take market share from Si Interposers in the future through innovative FO-on-substrate and FO-embedded bridge solutions.

TSMC is the market leader in high-performance FO solutions for high-end computing, networking, and HPC applications. ASE, SPIL, Samsung, JCET, Amkor, PTI, TFME, and Nepes are developing similar solutions with huge potential to compete. Though core FO is the primary OSAT market, the main developments are in HD and UHD FO technologies.

FOPLP has been hyped as the solution for the widespread adoption of FO, especially for large package sizes. However, it still presents technical challenges, and there is a lack of demand to achieve the desired cost benefit.

Yole Intelligence’s semiconductor packaging team invites you to follow the technologies, related devices, applications, and markets on www.yolegroup.com.