Figure 1 – OSAT Offering by Application and by Types of Packaging

OSAT stands for Outsourced Semiconductor Assembly and Test. This is a third-party service that suppliers around the world offer, which consists, as the name implies, of semiconductor assembly, packaging and testing of ICs (Integrated Circuits).

OSAT providers have an extremely important role in the semiconductor industry, now more than ever, due to the fact that they are the bridge that covers the divide between the semiconductor foundries and consumers.

OSAT vendors provide testing services such as: wafer test and final test. And in addition, assembly service such as: QFN, BGA, WLCSP and more.

As of 2020, the OSAT market is valued at $31.64 billion and is expected to reach $49.71 billion at a CAGR (Compound Annual Growth Rate) of 7.3% over the next five to six years. The increased demand from the Automotive sector and IoT (Internet of Things) connected devices are viewed as the main driving force in the foreseeable period.

OSAT companies are contracted by semiconductor design companies, such as Intel, AMD, Nvidia etc., and execute on those companies’ designs. Intel, for instance, is both a chip designer and a foundry (wafer provider) — due to the fact that they own and operate their own fabs or foundries. Intel outsource its chip packaging to various OSATs for assembly and test services — before they ship the chips to customers.

Figure 2 – OSAT Providers – Top 3 Major Players

The OSAT market is highly competitive, with a lot of companies vying for the top spots. As of now, China is an emerging market for OSAT providers and is also the largest market globally. This is due to the fact that the local government, recognizing the potential gains, offers incentives and support for local OSAT providers according to their “Made in China 2025” plan.

Here is a non-exhaustive list of OSAT providers:

Figure 3 – Distribution of semiconductor demand by end use worldwide in 2019

The smartphone segment has been the biggest source of revenue for OSAT providers, with more than 1 billion shipments every year. Recently, the market has become saturated and is declining. This segment still has a very significant role for OSAT players owing to the number of current smartphone orders. Furthermore, the introduction of the 5G technology is going to bring further profits to the market.

Figure 4 – Market Concentration

Another big segment is the industrial sector, of which connectivity has become the core in recent years. As such, the demand for edge computing and IoT devices is predicted to grow exponentially in the next ten to twenty years.

From the AI side, as there has been a widespread adoption of AI and other associated technologies, newer chips are being developed by smaller companies in the electronics market, which are lacking in infrastructure for testing and packaging, relying on OSAT to manufacture their AI-tailored chips.

Chip providers are forced to release new products within a short and limited window of time. The chip makers are also trying to integrate as many components as possible into a single chip, which has further increased the complexity and the time required to push out ICs. These designers are highly dependent on the OSAT providers for scaling their production to meet the current market demands.

Additionally, due to the high costs of building and then operating more massive production lines, manufacturers are more and more inclined to outsource their semiconductor assembly and testing operations to third-party providers so that they can focus more on their core operations of designing and engineering.

The outbreak of the COVID-19 pandemic has significantly disrupted the supply chain and production especially in the Asia-Pacific region, which is the largest market for OSAT companies. Most semiconductor manufacturing industries have been impacted by the fact that the Asia-Pacific region has become a world production center over the past twenty to thirty years. Owing to the labor shortages, many of the package and testing plants in this region have slowed or even halted operations creating a bottleneck for companies that depend on the OSAT providers’ services.

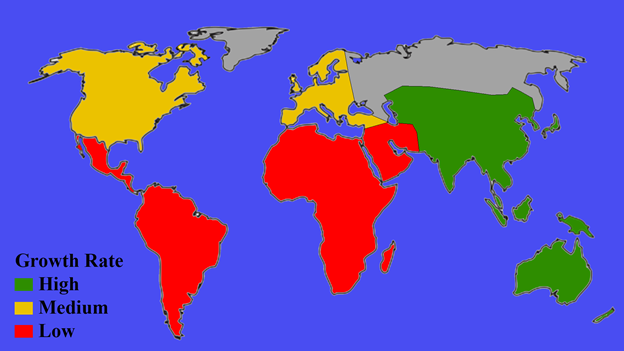

Figure 5 – Projected Growth Rate by Region 2020-2025

Throughout the automotive industry there is a constant shift towards more electronics and the semiconductor industry has mostly benefited from it. The number of electronics installed in an automobile system has gone up drastically, and one of the vital components of future cars is going to be the ADAS (Advanced Driving-Assistance System).

ADAS will have even more extensive penetration due to the new regulations by the EU and the US, where all vehicles are to be equipped with autonomous emergency braking systems and forward-collision warning systems. Also, the push for more renewable energy creates another potential profitable sector for OSAT vendors, as electric cars and renewable electricity generation systems are all going to require more electronics.

Besides traditional standard ICs, interest for ASICs is also growing fast, as they can be tailored to a specific application. One notable example is the development of the FSD (Full Self-Driving) Chip, of which there are two (for safety and redundancy) in each car produced by Tesla. It has been developed as a better alternative to the Nvidia GPUs Tesla was using before, which were not enough to achieve FSD in the timeframe imposed by Elon Musk, the Technoking of Tesla (CEO).

Many semiconductor companies who had traditionally stayed away from the Automotive sector are venturing into this growing market and OSAT players like Amkor Technology Inc. have set up dedicated facilities which cater only to the demand from the automotive sector.

The IC testing and packaging industry is predicted to register potential growth in China during the following 5 to 10 years, with the primary revenue driver being the increase in the amount of electronic components demanded by mobile devices. This active demand has also increased the deployment of advanced packaging solutions that provide higher integration levels and higher numbers of I/O connections, making chips both smaller and more complex at the same time.

The People’s Republic of China is home to three of the top-five largest smartphone companies globally, posing tremendous opportunities for semiconductor adoption, but also increasing reliability of the global market on Chinese manufacturing, which can be good for the profits of western companies, but bad in the long term if another pandemic or global disaster were to happen.

Taiwan is the home to companies like TSMC (Taiwan Semiconductor Manufacturing Company) and ASE Group, who have partnered with tech giants like Apple, Qualcomm, NVIDIA and AMD to assemble and test their chips.

Due to the 2020-2021 pandemic, the subsequent world-wide shutdowns of factories, the push towards online jobs and working-from-home becoming almost ubiquitous, the demand for semiconductors in general has skyrocketed, while the supply has lagged behind. Firstly, the move towards work-from-home policies generated an unprecedented wave of electronics purchases, which depleted the on-site inventory of most retailers. As such, more devices were ordered, theoretically solving the problem.

There was just one issue. The fabs or foundries, that are ultimately the source of all the electronics we use, were already operating at close to full capacity or were having issues with the personnel due to the pandemic. So the demand increased almost exponentially over a short period of time.

Secondly, compounding on all this supply shortage was the second wave of the crypto-currency bull market, which saw increased demand from miners of the new and better graphics cards and/or ASICs announced in 2020.

Thirdly, the automotive industry, following the sudden drop-off of car sales in March 2020 and the huge lay-offs in March, April and May of 2020, ordered fewer electronic chips and components for their cars. This was then followed by a resurgence in interest and sales picked up faster than predicted. As the foundries were already at their maximum capacity, car manufacturers had to sometimes halt assembly lines due to missing electronics, which were vital to the cars (like the ECU which controls the motor in ICE cars).

There were a lot more factors at play behind the shortage, but these three were the ones that caused the bulk of the problem. All of this has only helped to increase the importance of the role of OSAT providers in the current context and the following decade.

OSAT companies are now looking into expanding their current fabs and building new ones, but that is easier said than done, as these ventures cost a lot of money, in the order of tens to hundreds of millions of dollars, and take a long time. Also, those OSATs require ICs themselves, which need to be produced somewhere, too, which compounds on the already existing problem.

Get an indicative packaging cost range, then a detailed breakdown by email.