This is a guest post by PLDA which designs and sells intellectual property (IP) cores and prototyping tools for ASIC and FPGA

You are on a very strict schedule for your next chip. Not wanting to reinvent the wheel, you plan to go to an outside vendor for some of your

Read More

It’s no secret that Google, Amazon and Apple are heavily involved in the semiconductor industry. Apple itself is the biggest buyer of chips and estimated to buy 10% of chips sold worldwide. Google uses Intel’s CPUs in their server farms and represent alone 4% of Intel total sales.

Both

Semiconductor foundries claim they release a new technology node every two years. They may be off by a year or two, but on the whole, this is quite impressive, no doubt. Come to think of it, I don’t believe many of us even change our mobile phone every two years. How

Read More

The following infographics shows Synopsys’s mergers and acquisitions along the years from its very beginning. Synopsys was founded in 1986 by David Gregory, Aart de Geus and has been involved with many mergers and acquisitions.

The very recent large acquisitions include:

2008

Synplicity

ChipIT

2009

ChipIdea

Read More

The following infographics shows Cadence’s mergers and acquisitions along the years from its very beginning.

Cadence Design Systems was founded in 1988 by the merger of SDA Systems and ECAD and has been involved with 100 mergers and acquisitions. The very recent and large acquisitions are:

Year 2013

Tensilica

Read More

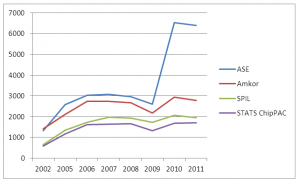

Semiconductor Assembly and Test Services are converting rapidly into a pure outsourcing mode of operation. While today perhaps only 50% of the market is using Outsourced Semiconductor Assembly and Test (OSAT, or SATS) this number is set to increase in the future.

While many of the low-end suppliers are