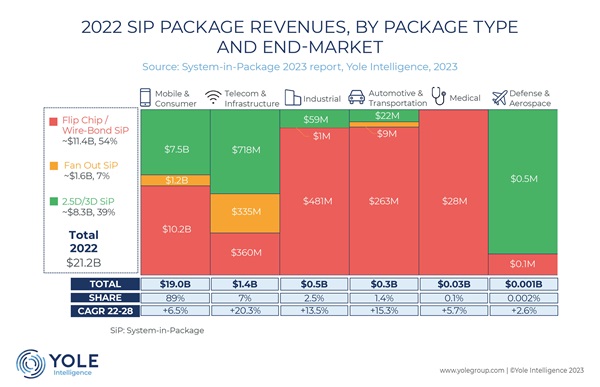

The SiP market was worth US$21.2 billion in 2022 and is projected to reach US$33.8 billion by 2028, growing at an 8.1% CAGR. This growth is fueled by trends like heterogeneous integration, chiplet technology, package optimization, and cost-efficiency, particularly in 5G, AI, HPC, autonomous driving, and IoT sectors. Yole Group’s analysts forecast that the mobile and consumer segment, which accounted for 89% of the 2022 revenues, will maintain a 6.5% CAGR, driven by 2.5D/3D technologies, HD FO , and FC/WB SiPs.

Yik Yee Tan, Ph.D., Senior Technology and Market Analyst, Packaging within the Semiconductor, Memory, and Computing Division at Yole Intelligence, part of Yole Group

“While mobile and consumer remain static in the overall semiconductor market, they are thriving in SiP due to 5G and computing trends. Telecom & infrastructure, automotive, and industrial sectors are the fastest-growing SiP markets, with telecom & infrastructure expecting 20.2% growth and automotive a 15.3% CAGR.”

In its new System-in-Package 2023 report, Yole Intelligence explores the SiP industry with market forecasts and trends.

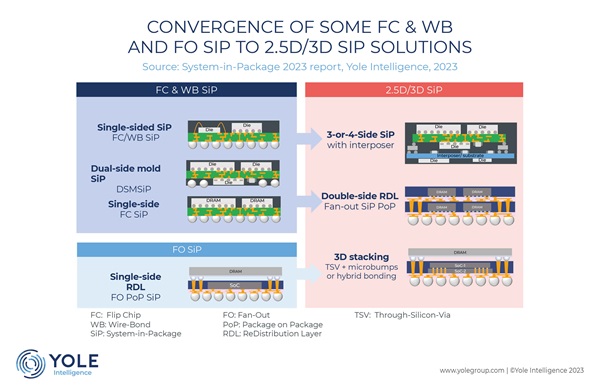

With this new product, the company analyses the related technologies and the trends toward 2.5/3D solutions. Indeed, SiP technology trends remain aggressive as the industry continues to demand more integration to allow reduced form factors and higher-performance products. In the mobile and consumer market, for example, footprint optimization is paramount because space is limited. This is particularly valid for smartphones, wearables, and other devices. For instance, the penetration of 5G in high-end smartphones has driven the adoption of SiP for RF and connectivity modules, with the need to integrate more components and shorten interconnections to achieve the required performance.

Furthermore, this new report includes specific sections focused on the adoption of these technologies as well as details of the ecosystem, including the supply chain, competitive landscape, and market shares.

Gabriela Pereira, Technology and Market Analyst, Packaging, within the Semiconductor, Memory, and Computing Division at Yole Intelligence

“The SiP market is intensifying competition as SiP technologies gain prominence due to chiplets, heterogeneous integration, cost optimization, and footprint reduction trends, attracting more entrants.”

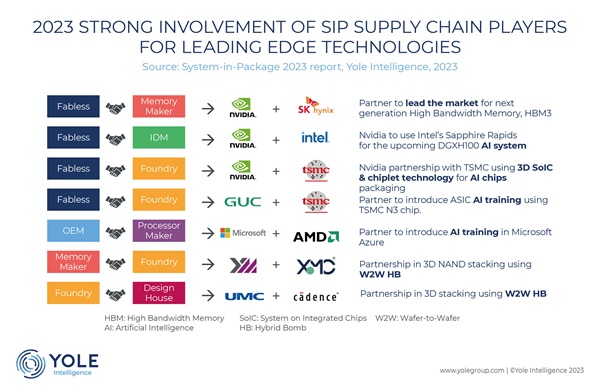

Indeed, the SiP supply chain is becoming increasingly competitive, and the focus is on collaboration for optimal results. More partnership between chip and memory players, foundries, and others are increasing, aiming to introduce cutting-edge technologies.

So, what is the status of each strategic region? Asia dominates the SiP market with a 77% share, with Japan leading at 41%, primarily driven by Sony’s 3D CIS market. North America holds 23%, thanks to contributions from Amkor and Intel, while Europe accounts for 2%.

From a business model point of view, FC/WB SiP is chiefly driven by OSATs like ASE, Amkor, JCET, TFME, PTI, Huatian, ShunSin, and Inari. TSMC dominates FO SiP with its InFO line, and Sony’s CIS market leads in 2.5D/3D SiP, followed by TSMC with Si interposer, Si bridge, and 3D SoC stacking.

To maintain competitiveness, companies explore M&As and capacity expansion, offering comprehensive solutions to reduce time-to-market. These trends span various SiP market segments, including IDM s, OSATs, foundries, IC substrate suppliers, and EMS. OSATs, comprising 32% of the SiP market in 2022, focus on full-turnkey solutions and plan to invest in advanced SiP offerings. IDMs, accounting for 48%, develop proprietary packaging technologies, while foundries, mainly TSMC, hold 17% with advanced assembly capabilities. IC substrate suppliers are entering the market, and EMS models are expected to grow, especially in wearables. China’s SiP market presence is expanding, with compatibility and interest in packaging technologies for chiplets and hybrid bonding to enhance competitiveness.

Yole Intelligence’s semiconductor packaging team invites you to follow the technologies, related devices, applications, and markets on www.yolegroup.com.